by Wajid Ali

Imagine yourself at a casino table clutching your last few chips. Every spin of the wheel or dice roll seems like a chance to recoup your losses—stirring a mix of hope and despair. This scenario, while dramatic, encapsulates a profound mathematical problem known as the Gambler’s Ruin Problem. It can not only describe the likelihood of you winning or losing your capital but has immense applications in evolutionary theory. The roots of this idea trace back to the work of 17th-century French mathematician Blaise Pascal.

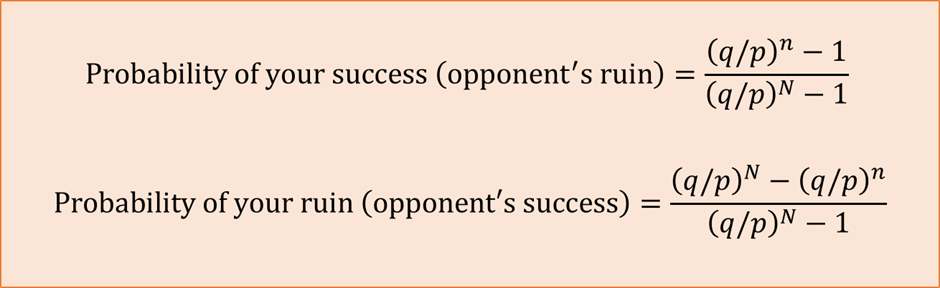

Let’s dive deep into your casino scenario. Assume that you start playing with an initial capital of n dollars and play against an opponent with m dollars (let m+n=N). The game stops if either of the player’s capital reaches 0 dollars or N dollars. The game progresses in stages, after each round your capital increases by 1 if you win (with probability p) and decreases by 1 if you lose (with probability q=1-p). The capital that you possess at each stage of the game is represented by a random walk on non-negative integers. This process has two killing states or absorbing barriers 0 and N which are referred to as the ruin of you and your adversary respectively. We see that when p>1/2 then you have the upper hand of wining and when p<1/2, a disadvantage of losing is evident. If you and your adversary have an equal chance of winning a round (i.e. p=1/2) then the probability of you ending up with a fortune of N dollars is proportional to your initial capital (i.e. n/N). However, when 𝑝 ≠1/2 then:

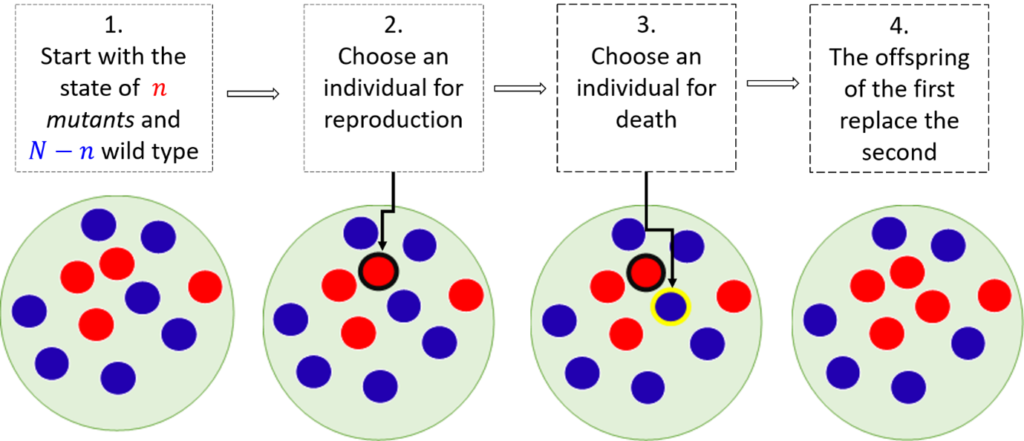

While the imaginary situation of your gambling may seem disconnected from the natural world, however, the principles governing it offer surprising insights into the theory of evolution. The probabilities of winning (or losing) mirror the genetic drift and fixation of alleles within a population. This connection was famously explored by Patrick Moran in the 1950s in his work on stochastic processes in genetics. Moran considered a finite population of haploid individuals, say of size N, in which n are mutants and N-n are of the wild type. When an individual dies the gap is immediately filled by an offspring of an individual from the pool of individuals before the death event. Think of the number of mutants as the initial capital and the population size of the population as your maximum fortune. The state of the system is described by the number of mutants at any given time. Similar to your capital at hand increasing (decreasing) on winning (losing) at each stage, the number of mutants may increase (decrease) with births (deaths). Note that the state of the system won’t change when the wild (mutant) type gives birth to a wild (mutant) type and replaces a wild (mutant) type. This resembles a draw in a given trial of a gambling game.

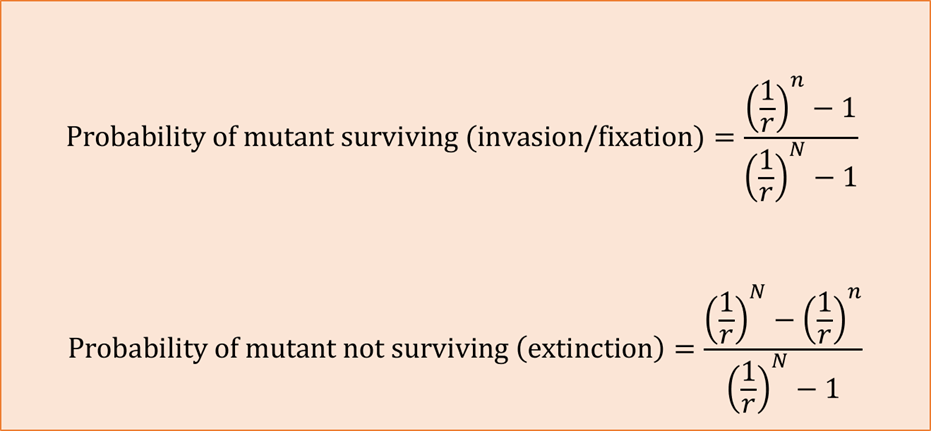

Let p be the transition probability of going from the state with n mutants to the state with n+1 mutants and q=1-p be the probability of transitioning to the state with n-1 mutants. There are two absorbing states with 0 mutants (extinction) and N mutants (fixation). The probabilities p and q may be thought of as being proportional to the finesses of the mutant and wild type, respectively. The ratio r=p/q represents the relative fitness of mutants. If r=1 then the probability of invasion is proportional to the initial number of mutants, that is, the probability of mutant surviving is equal to n/N. However, when r ≠1 then:

To sum up, the Gambler’s Ruin Problem—a variant of the classical random walk—offers a foundation that could be built upon in the investigation of more complex scenarios. Its applications extend beyond Moran’s model, influencing a wide range of problems in biology and social sciences.

References

Bailey, N.T., 1991. The elements of stochastic processes with applications to the natural sciences(Vol. 25). John Wiley & Sons. (Chapter 4)

Durrett, R. and Durrett, R., 199 9. Essentials of stochastic processes(Vol. 1). New York: Springer. (Chapter 1)

Feller, W., 1957. An introduction to probability theory and its applications. Wiley & Sons. (Chapter 4)

Edwards, A.W.F., 1983. Pascal’s problem: the ‘Gambler’s Ruin’. International Statistical Review/Revue Internationale de Statistique, pp.73-79.

Moran, P.A.P., 1959. The survival of a mutant gene under selection. Journal of the Australian Mathematical Society, 1(1), pp.121-126.